Prior Employer 401ks, Rollovers and Options

Don’t do what I did - always make a plan for your prior employer 401ks!

Have you done this one as well?

In the grand scheme of things, this probably isn’t the worst move, as there have been studies done on the best investment returns are often from people who literally forgot about them and just ‘left them alone,’ but there are some catches. At one point, I had no less than four prior employer 401ks just ‘out there in limbo’, one of which was over 10 years old. I’m pretty sure I’m not the only one out there, at least for those of us working in the majority of modern world realities without pensions, and where fewer and fewer of us may even have the option (or inclination in some cases) to stay at a single job for decades.

Expenses may change on leaving your employer and out of sight/mind isn’t always for the better

Looking back when I finally decided to ‘clean up’ my ‘orphaned’ 401k plans, it could have been worse, and I did (with the exception of my 10+ year old one I’d ignored forever) at least check on how/if the costs changed once I was no longer with that employer. In my case, it wasn’t bad - $100 a year or less in expenses across most of them, which I could live with, considering they all had $100K or more in them.

However - this is both employer and management firm dependent, and there are some unscrupulous firms out there charging excessive fees that can add up or even drain your entire account if left alone long enough. Not only can their administration fees be high but they may also invest in higher expense ratio funds, have no fiduciary responsibility to you (which means they do not necessarily work in your best interest - which can add up to yet more fees).

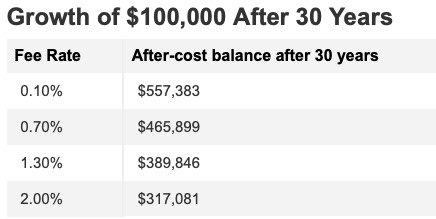

Even the base fees when employed may be higher than expected - compared to my paying $40/year for one account and $70 or so for another, one employment move had a 401K option which charged very close to .5% annually for ‘management.’ Considering a majority of us use target date funds as our core 401k investments, and a Vanguard fund doing the same can be had for .08%, this alone can add up over time to take away hundreds of thousands of dollars by the time you reach retirement!

Other downsides include lacking a single view of your retirement savings (same can also apply for investment, RSU and option accounts).

What are the options?

Well, there are a few:

-

Assuming your prior account has some minimum amount in it (usually like $5-$10K or so, you could simply leave it in place - but see the next section.

-

You can roll it over into a new employer sponsored plan with no tax implications to you. The old plan may be able to do an electronic transfer or may need to issue a check, either sent to you to then send on to the new plan administrators (you must do this within 60 days or face tax implications for cashing it out), or sometimes directly to the new administrators.

-

You can roll it over into an existing or new IRA account with no tax implications to you. The old plan may be able to do an electronic transfer or may need to issue a check, either sent to you to then send on to the new plan administrators (you must do this within 60 days or face tax implications for cashing it out), or sometimes directly to the new administrators.

-

Yeah, you could technically cash it out, but there will be tax and early withdrawal penalties that can be significant, as well as a potentially serious impact to your eventual retirement via lost compounding of gains and interest. Seriously, I know what it's like when you find yourself unexpectedly out of work, even down to having just purchased and moved into a new (used) house at the time. If at all possible, do not cash out your retirement savings.

So what ’should' you do?

Whenever you leave an employer, you should always check and confirm:

-

What are the administration expenses associated with the account now that you are no longer with that employer? Are they flat-rate or percentage-based?

-

What are the administration/management fees of your new employer’s provider? (if applicable)

-

Does the new fund have a suitable range of investment options for you, and what are their fund specific fees?

To rollover to the new employer, leave it parked, or roll it into an IRA?

Part of my eventual ‘cleanup’ to get my various funds/holdings/retirement savings in order I had decided to just roll them all into the new employers plan. After all, most of my prior employers has reasonably good low-fee 401ks, so this should be no different, right?

Not so fast. After I had closed out all my prior accounts and had checks issued to do rollovers with my new employers’ plan, I took a look ‘at the fine print’ for the new plan, and was shocked at their fees, as well as their online complaints, so I wound up having to put a stop payment on all checks for the rollover I thought I was going to do. Basically even their ~.5% as fees would have cost me thousands in fees if I had done the rollover, yearly, even before looking at the impact of reduced returns over time as a result.

So it did cause some delays on getting things sorted, needing to do the stop payment and check re-issuance, but it was sorted. In my case, I decided to go the new IRA account route. While there are annual contribution limits to personal IRAs ($7-$8K annually at time of writing, with a catchup/additional allowance if >= 50 years old), this doesn’t apply for rollovers.

Now, I did in this case decide to open a ‘managed’' IRA, but the fees are roughly in line with the half percent the employer plan wanted to do while adding zero value (employer plan), and I decided I’d let it roll for 1-2 years to then evaluate. I could have alternatively opened the IRA, done the rollover (which is now in cash), and selected a Vanguard or Fidelity Target Date all in one fund, or rolled my own allotment across US equity, Intl Equity, and bonds (something like 50% US VTSAX, or FZROX, then VTIAX or FZILX, etc. I am in fact doing just that but with the ETF equivalents on my taxable account, but again, I decided to give it a try to then come back, compare results in a bit and then possibly change. In general, there are lots of strong opinions on not going the route of managed accounts or even managed specific funds, but that’s something each person needs to decide on for themselves, considering their own personal risk level. One of the main reasons I think I decided to give it a try in this case is simply the usual target date funds are still pretty bond-heavy while the US bond market really hasn’t performed in some time. Now I could have effectively managed this myself by either selecting a further out target date fund (the further out your retirement or target date, the higher the concentration in stocks and equities and the lower in bonds), or rolling my own across multiple indexes and/or bonds, I’ve got several other accounts I already need to step up to keep in balance as well as adjusting over time. YMMV.

One last thing if you are going to do a rollover

This one may well depend on the type of account you’re rolling the older funds into, but always check. Even with something like an employer sponsored 401k plan, but almost certainly with an unmanaged IRA account, the newly rolled over funds need to be invested to benefit you down the road. Whether that’s via a single target date fund, individual holdings, and regardless of allocations - you need to be in the market to benefit, so make sure that your rolled over funds are actually invested. Occasionally there will be a horror story article about someone who thought they did everything right, executed a rollover, to then find a decade or more later that their funds were there, but sitting in cash uninvested. Don’t let this one be you. Of course, once everything’s tied off and you have confirmed the funds are transferred and invested appropriately, it’s worth checking in a couple of times a year just to ensure nothing strange has happened and see how things are going, but do make the effort during a rollover to make sure you see it all the way through.